By Chris Temple – Editor/Publisher

The National Investor

https://www.nationalinvestor.com/

(From the September 27, 2002 issue)

In addition to our regular Friday evening Metals, Money and Markets Weekly on kitco.com (at https://www.kitco.com/commentaries/2022-09-23/The-Metals-Money-and-Markets-Weekly-B-is-for-da-bears.html) I was party to two much deeper discussions late last week. They were:

*https://www.youtube.com/watch?v=ULJPc5M6AlY&t=123s – This was my latest discussion with friend and colleague Mike Fox on his The Prospector News podcast and

*https://relevantradio.com/listen/our-shows/the-drew-mariani-show/ -- Here, I was guest host John Harper’s guest last Friday afternoon (NOTE: You need to look for Hour 2 from last Friday the 23rd and click on it; I start halfway in or so.)

On both of these later discussions especially, I painted the bleak picture of the mess the Fed (chiefly) and the Biden Administration (a respectable second-place showing) have made of the economy and markets. It’s one that will be with us for YEARS in numerous forms. And all told, it suggests to me that the current bear market for the stock market, generally, is not at its ultimate end.

Technically, stocks scored a near-term victory at week’s end last week given that the S&P 500 (most important) and Nasdaq ended up above their June lows, even if the Dow Industrials did not. But yesterday (Monday) the S&P closed slightly below its 3666 marker from June. Ominously, Treasury yields that continue to violently ratchet higher aren’t doing the bulls a whole lot of good right now.

I’ve already shared my thoughts extensively in recent days RE: The Fed’s/Powell’s near “suicide mission” as I quipped last week. MAKE SURE you listen to those above-referenced discussions; that’s why I post them to social media as soon as they are available. In many ways the evolving stagflation, market shocks and the rest are going to be unlike anything we have seen before; and we’ll need to remain nimble.

Going into the latest F.O.M.C. meeting, my thoughts were tilting toward a better chance than not that we were at/near a low that could hold into early 2023. I still lean that way: but less so, given the much greater turmoil now in currency and credit markets. The odds that Powell and his merry band of monetary imbeciles are going to pull out one too many sticks are that much greater if they do follow through with another 75 bp and one 50 bp hike in the balance of the year. Perhaps they already have pulled out one (or more) too many and the consequences just aren’t here yet.

None the less, my views that we could get a more extended bear market/counter-trend rally begin with the following reasons/theses:

* “Peak Fed” – I think the worst we are going to hear from the Fed came last week. At long last—witness the major renewed spikes higher in Treasury yields and the greenback—markets are taking seriously Powell’s “hawkishness.” And that was the plan: before the Fed does anything more, Powell driving his purported inflation fighting seriousness home has quite quickly taken a bit more air out of still-inflated assets of all kinds.

I hardly believe—with commodity prices having caved a lot more, business slowing and the needs for retailers to discount a LOT of the crap they’ll be selling the hoi polloi over the balance of the year to get rid of bloated inventories—we’re going to get any more nasty hawkish surprises like last week’s. On the contrary: if the coming economic stats continue to be lukewarm to even negative AND the next couple inflation reports surprise on the downside, the dovish surprise for the balance of the year will be the Fed foregoing a further 125 bps of hikes in favor of 100…or less.

Mid-term election: The Establishment game has been ramped up here and there of overstating support many Democrat candidates have—and understating that of their G.O.P. opponents—in part hoping that fund raising in the home stretch to the latter will dry up. We’ll see. Odds still favor Republicans taking one or both houses; if the latter, that will cause stocks to rally, all else being equal.

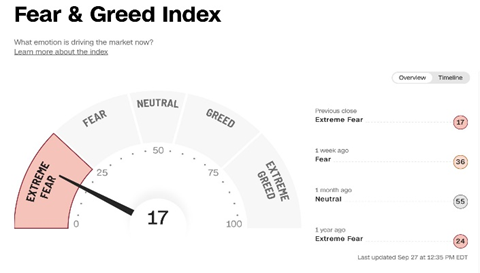

Bearish sentiment: Historically high levels of put option buying were evident late last week. This, together with $5 trillion-plus in “cash” on the sidelines, both point to a near-term bottom at hand, or one coming soon.

Indiscriminate selling, again: Last week’s bloodletting particularly claimed many victims among solid REITs, pipelines and many more companies that tend to get sold with other more worthy ones at the end of selling bouts.

Parabolic moves in dollar, rates are unsustainable: I said as this week got underway that these kind of moves, to me, suggest a bottom in days more than in weeks.

PORT IN A STORM—THE U.S.

But that said, let’s talk about the standout performance of the U.S. dollar; and the relative outperformance likely ahead of us of dollar-denominated assets compared to those in other developed (and the majority of undeveloped) nations.

As I recently said, that the dollar’s move has morphed a fair bit from one based on policy (the Fed’s greater hawkishness than other central banks, etc.) to fear of disasters elsewhere is a BIG danger. You have heard me warn before of the greenback’s surge in 2022 turning into a “dollar doom loop” – and we are precariously close to that type of phenomenon getting out of hand. When it becomes “run for the hills” time in the minds of many traders, they sell (risk assets and troubled countries’ currencies) first and ask questions later. The dough is by and large parked or repatriated into U.S. dollars. This can feed on itself and cause all sorts of trouble; and when (as with Monday this week) you see a near two-point gain in the U.S. Dollar Index, you know something may be about to break.

Hopefully, what that also means is most any day now there should be some relief given that these trades have become grossly overextended; at least for the time being. Barring one of Germany’s biggest banks going belly-up…Chinese President Xi really being overthrown…or nukes flying into and/or over Ukraine, I suspect that the “Peak Fed” thesis above—if given a little life, at least, with more slowing economic and then inflation numbers—could take rates and the buck off the boil.

But going forward, it seems almost certain that events will disproportionately favor dollar assets. Even when Treasury yields have peaked and come back down somewhat (more on that just below) it is most likely going to be due to recession/global market fears that will, net, still have more money going into the greenback than not. With U.S. markets and the economy here doing less bad than others, that should likewise limit declines for U.S. markets versus others; see https://www.bloomberg.com/news/articles/2022-09-12/goldman-s-kostin-says-us-economy-a-safer-bet-than-dire-europe?sref=AqatjHHy.

Of course, as I have already intimated a few times in the last several days, ALL this is a moving target. Our mix of directional trades may well change; so don’t go too far!

And please bear in mind that these thoughts cover the near term; perhaps into the early part of 2023. After (likely) a rally on hopes—or even the reality—of a Fed pause or pivot…a G.O.P. victory in the mid-terms…commodity prices staying down a spell…inflation halving to 4% or so by early next year…the reality of a secular bear market and stagnation will set in anew.

It won’t be like 1929 and into the 1930’s, necessarily. Nor like 2008. This likely years-long comeuppance will be combining an even worse global New Energy Crisis than the foretastes we’ve seen…with other intensifying commodity and currency wars and crises…a hunkering down of consumers that probably will rival the 1930’s…more political angst, as ever-more caustic (and as always, off point and diversionary) blame is tossed around for the deterioration of our way of life…debt defaults and repudiations…and last but not least, the greatest stress ever on U.S. global hegemony over most everything.

If we live through it all, the years ahead will be as fraught with investment opportunities as they are with peril.

If you want to roll up your sleeves and go through one of the most comprehensive takes on all this that Yours truly has read, check out https://www.hussmanfunds.com/comment/mc220925/. In this very well laid out piece (a far cry from the usual perma-bear scare tactics and sales pitches, all of which have been wrong for YEARS) John Hussman here clinically and piece by piece explains why our world is about to change in a BIG way; and why there is little left that central authorities can do to postpone the inevitable.